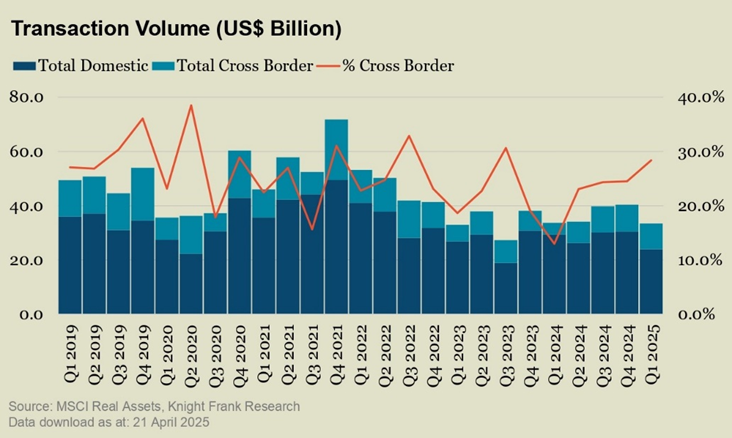

- Asia-Pacific real estate investment held steady at US$33.4B in Q1 2025, down just 0.8% year-on-year but 17.1% lower than Q4 2024, with cross-border deals making up 28.4%—the highest since Q3 2023

- Japan, South Korea, Australia: Continued investor favourites, with Japan leading activity on currency advantages, South Korea’s industrial resilience, and Australia’s retail rebound

- Malaysia: While still an emerging player, Malaysia is drawing cautious interest for its competitive yields, improving transparency, and specific sector strengths in Greater KL, Penang, and Johor

Kuala Lumpur – Knight Frank’s latest Asia-Pacific Capital Markets Insights report reveals that cross-border investment in the region’s commercial real estate sector surged to US$9.5 billion in Q1 2025, doubling year-on-year. While Japan, South Korea, and Australia led inbound flows, Malaysia is cautiously emerging as a diversification market for global investors seeking value beyond mature hubs.

Keith Ooi, Group Managing Director of Knight Frank Malaysia, says, “We’re observing early signs of revived cross-border investor interest in Malaysia, particularly among those reassessing Southeast Asia’s growth potential. Malaysia offers improving fundamentals, an evolving REIT market, and increasingly transparent regulations. While investor caution remains, the region’s overall momentum offers reasons for optimism.”

Although Malaysia was not among the top cross-border capital destinations this quarter, Knight Frank notes a steady rise in enquiries, particularly targeting Greater Kuala Lumpur, Penang’s industrial corridors, and Johor’s logistics and residential hubs.

James Buckley, Executive Director of Capital Markets – Investments at Knight Frank Malaysia, adds, “Investors who once focused only on core markets are now eyeing Malaysia, albeit carefully. The industrial and data centre sectors are attracting funds as are hotels, given the rebound in tourism which is leading to improved occupancy and average daily rates. We’re seeing exploratory interest that could convert into transactions if key policy and macro indicators stabilize.”

Local challenges amid global uncertainty

While Malaysia benefits from a robust logistics and manufacturing base, affordability, and regional positioning, challenges persist, including currency volatility, evolving regulatory frameworks, and an oversupply in selected sectors like retail and residential. Knight Frank anticipates stronger activity in the second half of 2025, contingent on stable economic conditions and clearer government policy signals.

Overall transaction volume in Asia-Pacific held steady at US$33.4 billion in Q1 2025, easing 0.8% from the same period last year. However, it showed a sharper 17.1% decline from the strong activity in Q4 2024. International investors remain active, with cross-border transactions accounting for 28.4% of all investment activity, the highest proportion since Q3 2023.

Craig Shute, CEO, Asia-Pacific, Knight Frank, says,“Asia-Pacific’s real estate market held up well in 2025, with cross-border investment activity reflecting sustained interest, particularly in Japan, Australia, and South Korea. Stabilising asset prices and the clear signal that interest rates have peaked encourage investors to support renewed capital deployment. As investors gravitate toward office, industrial, and retail assets that offer resilient income and long-term growth potential, improved financing conditions and clearer valuation floors are helping to restore confidence across key markets.”

Christine Li, head of research, Asia-Pacific, Knight Frank says, “While we anticipate this positive momentum to gather pace, the on-again, off-again tariffs are muddying the outlook for further recovery in the investment landscape. Should tariffs lead to a sustained increase in inflation, the Fed would likely raise interest rates, exerting upward pressure on long-term interest rates and cap rates, potentially dampening capital markets activity globally. If implemented in full force, the industrial and retail sectors will likely bear the brunt, with decreasing consumer spending and shifting goods movement directly influencing demand.”

Despite the broader economic uncertainties, the office sector across Asia-Pacific demonstrates notable stability, protected by a unique combination of structural advantages and positive market cycles. This is particularly evident in Japan and Australia’s premier cities, where high occupancy rates persist alongside steady rental growth trajectories even as other sectors face potential headwinds.

More on the insights here: Asia-Pacific Capital Markets Insights Q1 2025

Legal Disclaimer: The Editor provides this news content "as is," without any warranty of any kind. We disclaim all responsibility and liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. For any complaints or copyright concerns regarding this article, please contact the author mentioned above.